AAB Wealth / Blog / Three scenarios where financial planning can make a big difference

Three scenarios where financial planning can make a big difference

Financial advice isn’t just for those about to retire. Whatever stage of life you’re at, you can benefit from greater clarity on the road ahead. Here are three scenarios that show how financial planning can help you no matter where... Read more

Financial advice isn’t just for those about to retire. Whatever stage of life you’re at, you can benefit from greater clarity on the road ahead. Here are three scenarios that show how financial planning can help you no matter where you are in life.

It’s never too early to seek out advice.

While many people start thinking about financial planning when they see retirement on the horizon, there are many other times in life when that support might be welcome.

At AAB Wealth, we help clients at many different junctures of their lives. Some are fairly close to retirement or, at least, thinking about slowing down. But others are still firmly in the ‘wealth accumulation’ stage, at their peak earning power, and want advice on how they can make the most of their current situation for the future. Whichever point you’re at; financial planning helps in many ways, not least when it comes to giving you more clarity on major decisions.

Here are three examples of financial planning in action:

1. Just getting started

Ciara and Stephen have recently become empty nesters.

Their children have moved out, with their youngest daughter about to graduate from university. In the next three years or so they hope to pay off the mortgage on their £750,000 home, freeing up around £2-3,000 disposable income each month. Their combined private pensions are worth more than £1 million.

They plan to retire in 10 or so years. But the dream scenario is not to be working flat out during that time. They’d like to wind down, perhaps go part-time, and take more long-haul holidays.

However, at the same time, they know they may still need to support their children while they find their feet, for example, by helping them get on the property ladder. They want to know if they can do both, without running out of money in later life.

We can help Ciara and Stephen so that they:

Can see that if they do reduce their working hours in the future, they have enough capital to draw upon to support both their lifestyle and their children’s needs. They can see at which point they could start to work less, and how that would impact things.

Know when they can help their children onto the property ladder with a deposit without compromising their own financial security.

Feel confident that they can sustain their lifestyle in retirement while also being able to meet any unexpected costs.

How do we do this?

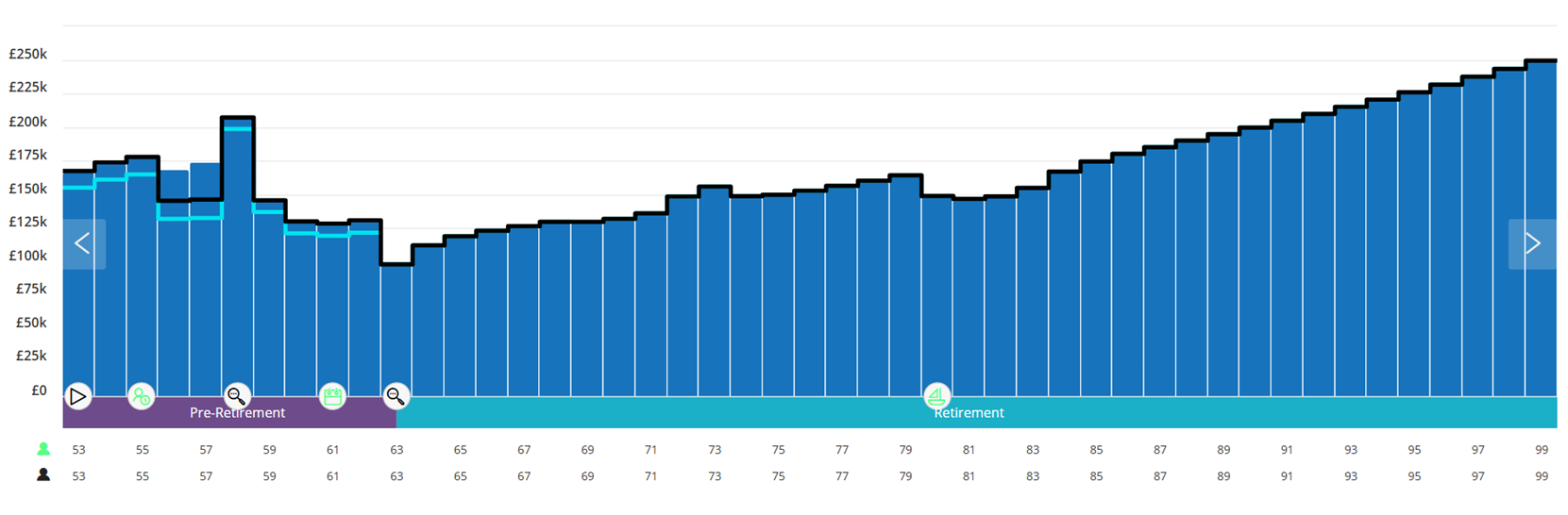

We use something called Cashflow modelling, which lets you visualise your income and expenditure in different scenarios and shows you how it plays out over time. This enables us to model various “What if?” scenarios before you need to make any decisions. You can see below how this can bring things to life and provide reassurance around key decisions.

The first graphic shows Ciara and Stephen’s current situation – they’re spending £65,000 each year (evidenced by the black line, which shows this spend plus any taxes) but they will run out of money at age 92.

The second chart shows their situation after we helped them. They’re still able to spend £65,000 each year, plus any incurred taxes, but instead of running out of money, they have enough to last to age 99. But we’ve also factored in:

An additional £10,000 a year to spend on holidays, every year, between now and age 80

A gift of £40,000 to each of their two children as a house deposit in five years’ time.

A decrease in their working hours to 3 days a week in 5 years’ time, before fully retiring in 10 years’ time.

This was achieved by:

Restructuring Ciara and Stephen’s existing pensions to reduce costs and amend the level of risk being taken, to ensure they were invested appropriately for their risk profile and objectives.

Increasing contributions to their pensions between now and retirement to ensure their pension pot is substantial enough for retirement.

Being able to plan ahead gave Ciara and Stephen options that would help them achieve their long-term goals.

There are other scenarios where this can help others too.

2. Business owner

Jack is 60 and is selling his stake in the manufacturing business he co-owns with a partner for around £2 million. He wants to use some of the proceeds to pay off his current mortgage (he has around £200,000 left to pay) and buy a second property in France for around £1 million.

He hopes this property can be a combination of a holiday home for him a few months every year, a source of extra income if he lets it out as an Airbnb, and will supplement his income if he sells it later into his retirement.

We can help Jack to:

Understand the impact of buying the property, knowing that it means £1 million less in his investment pot, and feel confident in his decision based on his long-term spending plans.

Ensure his pension and investments are structured in a way that allows him to retire comfortably, even after his property purchase.

Plan ahead for the tax implications of selling his French property in the future, so there are no surprises down the line.

3. The retiree

Justin and Bella retired three years ago. They both have private pensions they’ve yet to tap into. Instead, they’ve drawn an income from a joint collective investment account, valued at around £500,000, and ISAs valued at around £150,000.

With a new grandchild on the way, they’ve decided to reassess their spending plans. They were already considering downsizing and selling their four-bedroom home in a few years’ time. But they now want to bring this forward, so they can enjoy being closer to their growing family.

They also want to revisit plans for their pension. Their original strategy was leaving this for others to inherit, as this was a tax-efficient means of passing on their wealth. However, with the government considering removing the exemption of pensions from inheritance tax, this is unlikely to be the case in the future.

We can help Justin and Bella to:

Optimise how they draw down their post-retirement income, ensuring they have enough to support their lifestyle while making the most of tax efficiencies.

Understand the tax implications of selling their home, so they can plan ahead with confidence.

Assess how downsizing impacts their overall spending plans and create a strategy to manage any additional capital in a way that supports their future goals.

Review their inheritance plans in light of the changes to pension tax rules, ensuring they can still pass on their wealth in a tax-efficient way.

The big question from every client seeking advice is always “What if?”

What if I decided to switch strategy, stop working, take a year out, move location, or something unexpected happens? That’s where financial planning comes in. Find out more about how we help in these scenarios in this video, with one of our Chartered Financial Planners Claire Marston.

You can also read more case studies on our website to find out what other circumstances we’ve helped people find clarity around their financial future. Perhaps there’s someone in a similar situation to you?

If you own a family business don’t forget these 5 important rules

Family businesses are the lifeblood of the UK economy. Working alongside your partner or children can be rewarding and even bring tax advantages. But running one is a delicate balancing act, with emotional ties that sometimes prove complex to unravel.... Read more

Elections don’t have to spell panic for your portfolio

Is a Labour or Conservative government better for my investment portfolio? Will markets crash if Donald Trump gets into the White House? 2024 is a year of big elections, but they might not have the impact that you think. This... Read more

Important changes to your National Insurance contributions

AAB Wealth would like to make you aware of an upcoming change to the rules concerning the purchasing of voluntary National Insurance contributions. A person typically requires 35 full years of National Insurance contributions to be entitled to a full... Read more