AAB Wealth / Blog / Market volatility and why it’s wise to stay the course

Market volatility and why it’s wise to stay the course

History shows us that market volatility is always with us. It’s not a signal that something is broken – it’s simply the market doing what it has always done… It’s been another bumpy start to the week for markets. The... Read more

History shows us that market volatility is always with us. It’s not a signal that something is broken – it’s simply the market doing what it has always done…

The S&P 500 index, which tracks the largest US companies, opened down 1.1% on Monday after US President Donald Trump suggested that new tariffs could hit all countries. Tech stocks were hit particularly hard: Nvidia dropped 3.7%, while Tesla fell more than 5%, facing pressure from falling sales, rising Chinese competition, and wider political backlash.

With headlines like these, it’s no wonder investors will be feeling nervous.

But as unsettling as these drops may sound, they are part and parcel of investing. Volatility isn’t a sign that something is wrong – it’s a feature of the market, not a flaw. And while the reasons for short-term falls change – whether it’s tariffs, inflation, politics, or corporate news – the pattern over time remains remarkably consistent.

This is why our advice remains the same: keep calm, do nothing. Of course this may sound counter-intuitive, particularly if you’ve only recently begun your investment journey; staying put might feel incredibly unnatural. But in fact, this is exactly what your financial plan was built for.

And why it may feel as if this is “different” or that something new is happening, history shows us that volatility is always with us. It’s not a signal that something is broken – it’s simply the market doing what it has always done: reacting in the short term, before recovering in the long term.

The long view

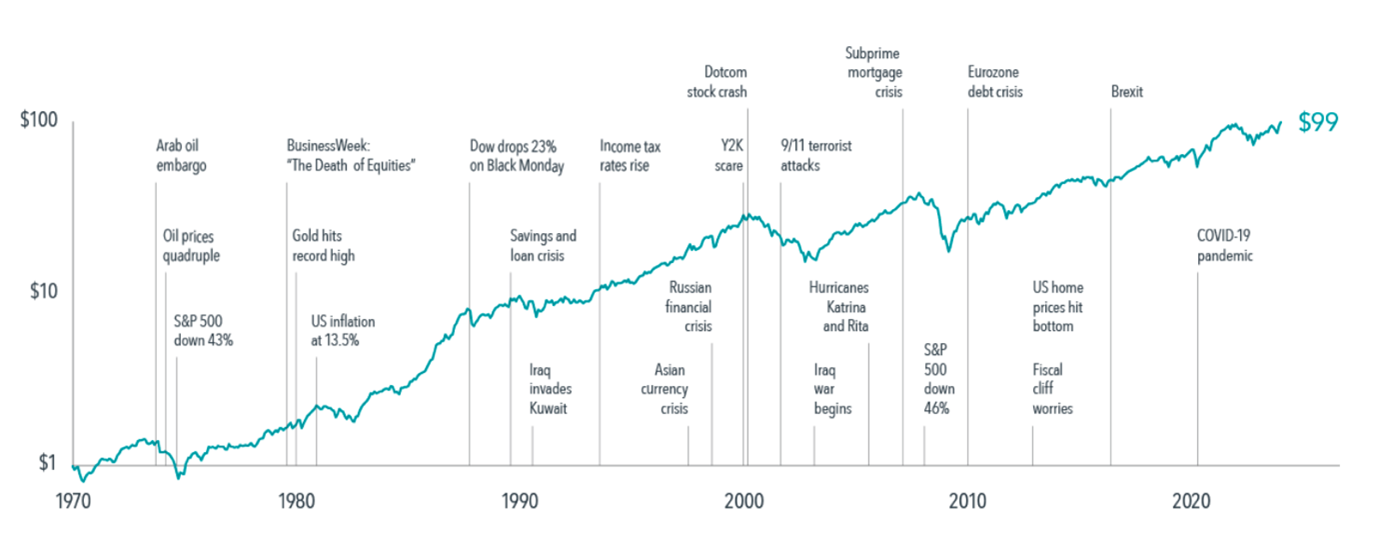

Take a look at this chart, which shows the performance of the US stock market from 1970 to 2020.

Growth of a Dollar— MSCI World Index (Net Dividends) 1970–2023. Source: Dimensional

Each of the dips along the way – from the oil crisis and Black Monday, to the dot-com crash, the global financial crisis, and even Covid-19 – felt like “this time it’s different”. But in every case, the market recovered. In fact, if you’d invested $1 in 1970, and held your nerve through every one of these crises, you’d have ended up with $99 after 2020.

What would be the consequences of reacting, you might be wondering?

Timing the market: the risk you don’t see

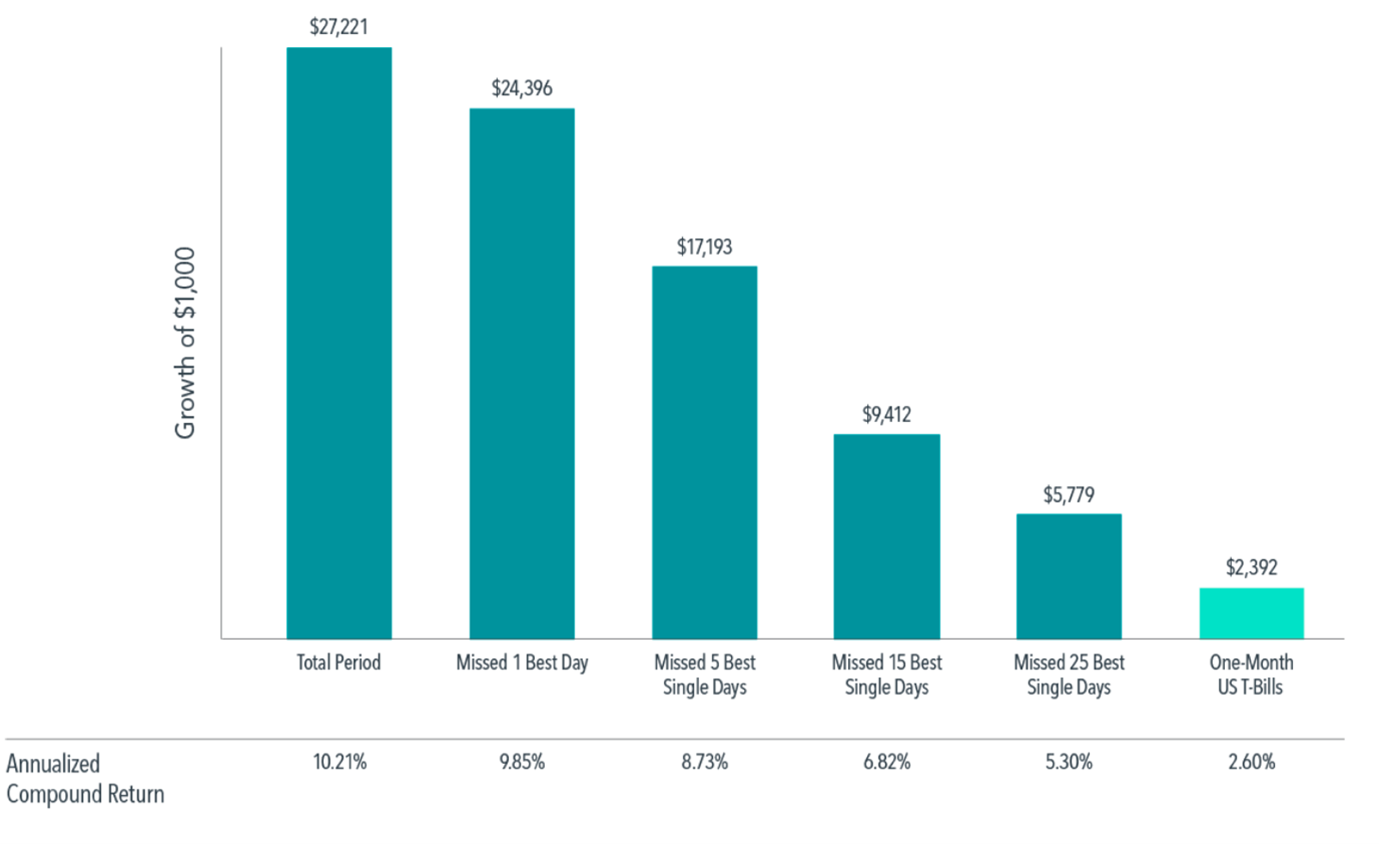

It might feel like the best solution is to try and protect your money by getting out. But as this second chart shows, missing just a few of the best days in the market can dramatically reduce your returns.

S&P 500 Index Performance Based on Time in the Market 1990–2023. Source: Dimensional

If you’d invested $1,000 in the S&P 500 in 1990 and done nothing, you’d have ended up with over $27,000 by the end of 2023. But miss just one of the best days? That drops to $24,396. Miss five, and you’d have lost more than $10,000 in gains.

This is why we encourage clients to stay the course. Because attempting to ‘time the market’ is more likely to cause harm than good.

Focus on what you do know

Now that the Spring Statement has passed – and thankfully brought no changes to tax or pensions – there are at least more knowns to work with.

While the Chancellor was clear this wasn’t a full Budget, the update still included some notable points:

Tax thresholds will remain frozen, meaning many households will feel the squeeze in real terms.

Public spending cuts and defence investment increases were announced.

Inflation is expected to ease back towards target over the next two years.

Interest rates have come down three times since the election – a possible sign of returning stability.

But even as economic indicators improve, market noise remains ever-present – especially when global politics and tech headlines collide.

That’s why we advocate for staying grounded in your personal financial plan – not reacting to headlines or predictions. As we wrote here, focusing on the knowns is far more useful than guessing the unknowns. And as we explored here, there’s no secret knowledge or group of people who can see into the future to predict what’s going to happen, however much they might try and persuade you otherwise.

Your plan is built for this

Your financial plan wasn’t designed for perfect conditions. It was designed to withstand market wobbles like this.

It includes:

Diversification across different assets

An emergency fund to avoid needing to withdraw from investments at the wrong time

A cashflow plan that helps you see the big picture, not just this month’s news

If you haven’t revisited your cashflow modelling recently, now might be a good time to do so. It’s a powerful way to visualise how short-term volatility fits into your long-term goals.

Beware the noise – and the ‘finfluencers’

Periods of market stress also bring a wave of unsolicited advice. The modern-day equivalent of the man down in the pub now has a TikTok account and a YouTube channel – and might sound very convincing. But just because someone has a platform, doesn’t mean they have a plan.

Resist the urge to follow unregulated, unqualified voices. If anything you read or hear makes you feel panicked or pressured to act, it’s time to pause, and talk to us instead.

We’ll be writing more about common behavioural biases in our next post – those emotional shortcuts that can lead us astray. For now, just remember: it’s human to feel anxious. It’s human to want to act.

But it’s wise to stay the course. And if you need help staying grounded, that’s what we’re here for.

After weeks of speculation, we finally know what Labour plans for the year ahead. But what do the Autumn Budget announcements mean for you? We’ve looked beyond the headlines at four typical scenarios to bring these changes to life. After... Read more

What does Labour’s election win mean for your financial plan?

It’s all change at the top. After a landslide win in the UK general election, there’s a new party in charge. So what kind of policies are we likely to see from the new Prime Minister? And what does it... Read more

Three key points from the Chancellor’s Spring Budget

Jeremy Hunt says he wants to keep taxes low and boost investment in British business. So what will his latest plans mean for your finances? We’ve picked out some highlights for you to consider from the latest Spring Budget. No... Read more

Why inheritance tax isn’t the villain it’s made out to be

Inheritance tax is ‘the most hated tax in Britain’ – many are likely to be relieved, then, to hear that the government is considering abolishing the tax if they win the next election. Although the Chancellor made no new announcements... Read more