AAB Wealth / Blog / It’s summer holiday time. How to make the most of ‘now’

It’s summer holiday time. How to make the most of ‘now’

Financial planning shouldn’t just prepare you for the distant future, it should also help you to enjoy the special moments that come along the way. Holidays don’t come cheap… This summer, UK holidaymakers are steeling themselves for costlier trips abroad.... Read more

Financial planning shouldn’t just prepare you for the distant future, it should also help you to enjoy the special moments that come along the way.

Holidays don’t come cheap…

This summer, UK holidaymakers are steeling themselves for costlier trips abroad. Thanks to a stronger pound against currencies in some of the more popular tourist hotspots, the average budget for a short break has shot up to £369 (up £59 from 2022), while a longer trip overseas is expected to cost £669 (up £231 from two years ago).[1]

Flights are also more expensive, a result of increased demand and higher taxes on jet fuel. This is particularly true in Europe where prices are now 15% above inflation.

If you’re planning a staycation, there’s not much respite either. As this survey from Which? shows, days out are much more expensive than they used to be. Many of the top tourist attractions, including Madam Tussauds, the Tower of London, and London Zoo, now cost around £30 per person.

Even a visit to an ice cream van will set you back more. Ice cream has gone up 45% in the last three years.

If this sounds a rather frivolous subject for a financial planner to tackle, it’s really not. Because, as much as we’re here to support our clients as they prepare for distant life stages such as retirement, successful financial planning lets you enjoy what’s happening now too.

A leap of faith

So, let’s talk about that holiday.

It’s a chance to switch off, recharge. Even if you’re only clocking off for a week or so, there’s a sense of letting go – at least for a short time, before picking up where you left off.

In some respects, it’s almost like a mini retirement. And this can be unnerving for some. Breaking deeply engrained saving habits, even if just for a moment, can seem like a big leap of faith.

Especially with the rising prices we’ve mentioned, you might be concerned a holiday could derail your carefully thought-out long-term spending plans.

That’s why many conversations we have with our clients are about striking a balance.

Helping get the balance right – cashflow modelling

On the one side, there’s growing your wealth for the long term, making sure it doesn’t get eroded by inflation.

But on the other, it’s important to have money that’s accessible to enjoy when you need it. Money that’s kept as cash, or in a short-term pot that’s relatively liquid and easy to get to when you need to.

We like to think of it in terms of “saving to spend”.

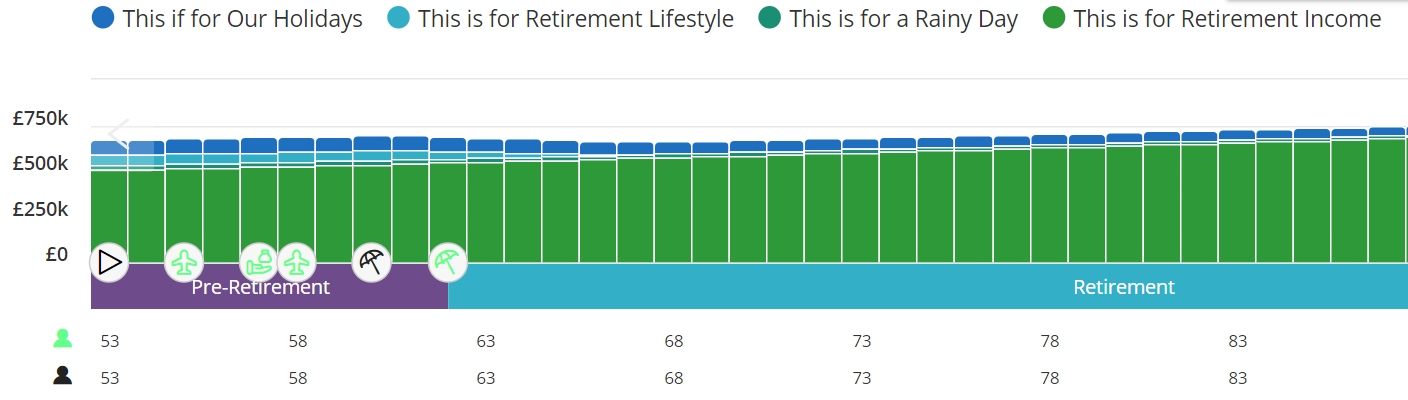

The best tool we have to help support you in this is cashflow modelling. This can help you visualise your finances and let you plan for different scenarios and the sacrifices you might need to make. You can even label different funding streams – “This is for our retirement,” “This is for a rainy day,” “This is for the holidays.”

In the example graphic below you’ll see how this looks. As well as a growing long-term fundyou can see that there are funds that can be used in the short-term for things like day-to-day spending and holidays.

We all get to be the grasshopper sometimes

Everyone’s attitude to money is different. We often find when speaking to a couple that one partner is more saver, the other more spender. It’s possible though to be a bit of both.

In the Aesop’s fable “The Ant and the Grasshopper,” the lazy grasshopper spends all summer playing, while the studious ants save up their food to survive the winter. The poor grasshopper has to beg the ants for help when the colder weather comes.

The moral of the story is clearly to be more ant than grasshopper.

But it’s ok to be the grasshopper sometimes, albeit temporarily. Saving doesn’t have to be all about the way off. In fact, with careful financial planning it’s possible to make the here and now more enjoyable too.

Asking these 5 big questions? You need a financial planner

Seeking advice isn’t just for the super-rich. And it’s not just selling you investment products. If you’ve never talked to a financial planner, you may be unaware of what we do and the important questions we can help you answer.... Read more

Two important lessons we can learn from the ‘everything rally’

Market commentators feared the worst for 2023. But despite global uncertainty, the predicted slump turned into the ‘everything rally’ – a surprising surge taking in stock and bond markets. Here are two things it can teach us when it comes... Read more